How to create a portfolio of compounders

July 26, 2025

Much has been written about so called 'compounders': companies with sustained high returns on invested capital. That grow and keep growing in a stable way over the long term. Usually due to network effects, due to scalability, due to the fact that they have a unique 'Moat'.

Get those two ingredients right and the math takes care of itself: every euro the business keeps gets recycled at a superior rate, expanding the profit snowball year after year. As Royce’s small-cap team puts it, a consistently high ROIC “means that management is effectively allocating capital.”

So should we look for these types of companies? Will they provide a high return for you as an investor?

Surely it is pretty juicy to invest in that multi-bagger compounder. I mean imagine investing in Walmart 20 years ago, or Costco, or Google, or Microsoft. That would have given you some good returns. It sure sounds promising.

Besides, there is a Morningstar Wide Mode index, MSCI Quality index. Furthermore, some equity funds focus on this exclusively. In Europe, there is Silvercross investment management. Perhaps you have seen Long Equity on X.

Let's run some tests today.

Our ingredients will be:

Compounding wishlist

- Stable (long term) revenue growth. We want the be able to draw a line through the Sales figures.

- Stable gross profit growth.

- Stable operating income growth

- Stable free cash flow growth

- High operating income margins.

- High ROIC. We want high returns on invested capital (that well exceed its costs of capital).

- Stable ROIC. It shouldn't change too much from year to year.

- Increasing ROIC. Als known as high ROIIC.

- Stable interest expense. We don't want any surprises when it comes to the debt position.

- Stable retained earnings growth.

- High retained earnings to assets.

- Stable ROA, ROI and ROE growth. We want to see a stable growing return on assets, investments and equity.

- Stable decline in number of shares. This means the company is buying back shares while earning a high return on invested capital.

- Stable operating cashflow to employees growth. We want the company to be scalable, not only in terms of assets, but also in terms of its employees.

- High operating cashflow to total debt. Keeping debt low means interest costs will be low and will not get in the way with the compounding process (of sustained high ROIC compared to costs).

- We will throw in some other metrics as well to make sure the company isn't too much overvalued, like high operating income to EV and Earnings Yield and FCF yield. And an accrual measure, which looks at the difference between net income and operating cashflow in the last twelve months and normalizes it to total assets. Lastly, lets throw in a measure that looks at the stability of working capital (like accounts receivable, cash, accounts payable). We don't want to have those fluctuate too much.

Putting it to the test

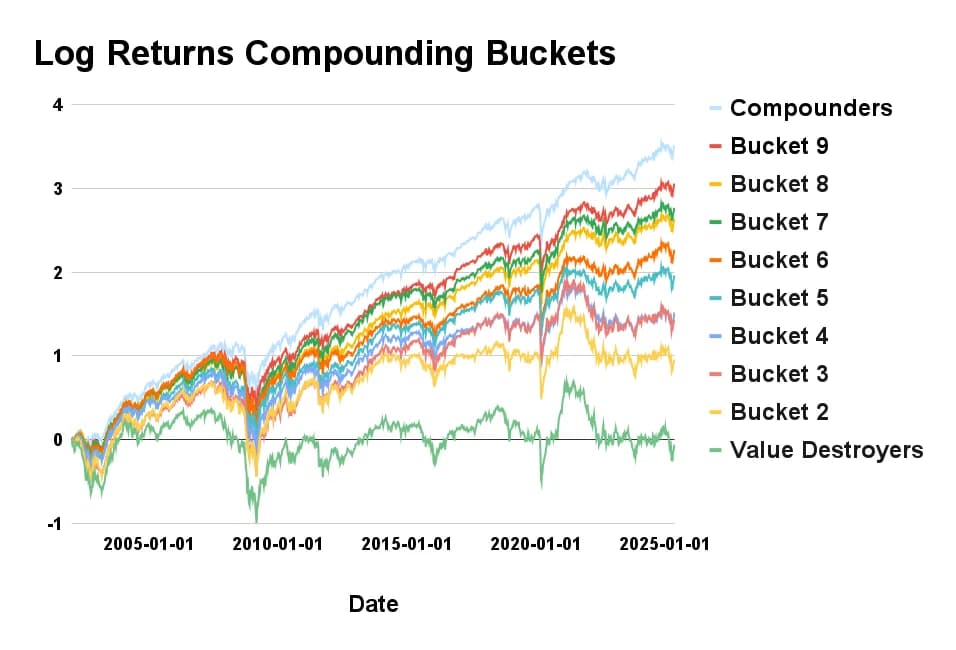

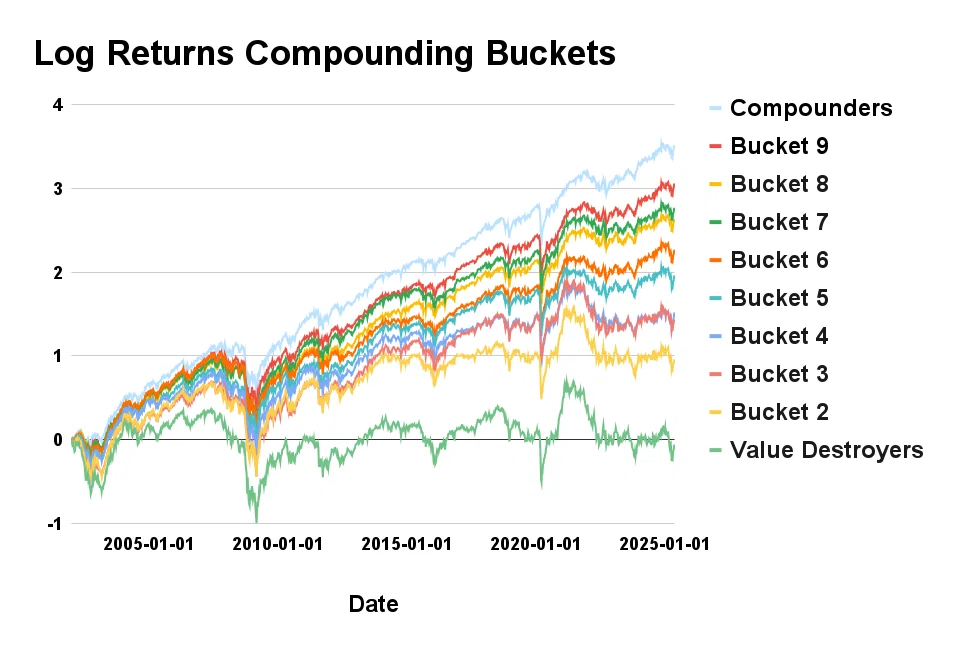

Let's use these measures and for each one of them, rank the companies against companies in the same Universe, Industry and Sector (such that each measure is used three times).

On a Universe with companies having more than 50.000 in median dollar volume each day (for the past half year), we get the following.

As you can see, it is pretty clear that it is better to buy companies that indeed look like a 'compounder' than the opposite - here coined as a value destroyer.

To determine stable revenues, growth profit and all the rest, we used the same formula that we used in a previous blog about long term stable growth.

What companies pop up?

Well, as of today, some companies in the top - that score highest on the metrics we listed before, are well known names. For example, ADBE is up there, MSCI is there and GOOGL as well.

But theres also some lesser known names. For example, Watts Water Technologies, Inc. (WTSS) scores really high.

Watts Water Technologies, Inc. engages in the manufacture and provision of products for water conservation, safety, and flow control. It operates through the following geographic segments: Americas, Europe, and Asia-Pacific, Middle East and Africa. Its services include plumbing and flow control solutions, water quality and conditioning, water reuse and drainage, heating, ventilation, and air conditioning, and municipal waterworks. The company was founded in 1985 and is headquartered in North Andover, MA.

WTSS description.

As does Cintas Corp (CTAS).

Cintas Corp. engages in the provision of corporate identity uniforms through rental and sales programs. It operates through the following segments: Uniform Rental and Facility Services, First Aid and Safety Services, and All Other. The Uniform Rental and Facility Services segment consists of the rental and servicing of uniforms and other garments including flame resistant clothing, mats, mops and shop towels, and other ancillary items. The First Aid and Safety Services segment includes first aid and safety products and services. The All Other segment contains fire protection services and its direct sale business. The company was founded by Richard T. Farmer in 1968 and is headquartered in Cincinnati, OH.

CTAS

As well as quite some other names, like DSGX, RSG, USLM, CMG, ADP, GWW, which I will leave you to look up (if you enjoy that).

So should we focus on 'Compounders?'

Well, if you are only focussed on returns, we can probably do better than this. We could add other metrics that increase returns as well. Perhaps some sentiment characteristics. Low short interest. Or perhaps some more valuation metrics. We can do way better than that, upwards of 50% returns per year on Universes that are less liquid.

Having said that. There are worse ways to invest.

Over the last 5 years I have made 40%+ returns annualized. Some of my current holdings are NATR, OOMA, EVS (Belgian company), STRT and ELMD.

More Post

Forging Your Own Path

Congratulations on securing the Full Book—your strategic blueprint for financial mastery. Within these pages, you’ll discover actionable insights and innovative strategies that redefine your investment approach. Ready to push further? Explore our Rankings page to uncover elite performance benchmarks, or dive into our Algorithms page to harness advanced, data-driven insights that give you a competitive edge. Your journey to transforming knowledge into extraordinary returns begins now.

The Best No-BS Factor